Share this post

Not all that glistens is gold

February, 2022

Many investors have become obsessed with interest rate rises in the short term and on how this affects the valuation of a company. We have written many times over the past decade that until interest rates provide, or are forecast to provide, a positive real return on a multi-year basis, not a lot has really changed in the Investment world. The reason for this is that any investment (cash being one) Is either held for safety/ emergency or held for its future intrinsic value.

During periods such as through January, investors focussed on the short term at the expense of the longer-term opportunity. Strong longer-term returns are driven by two relatively simple, but important, factors: the growth in free cash flows a business generates, and the price you pay for a share of those cash flows today.

We maintain these are relatively simple, but they can be confused and complicated by investors. In simple terms, a company must make a profit from which it can generate excess cash above its costs for maintaining and growing that profit in the future. Do this consistently and you are in the top 20% of global companies statistically. We know many examples of exciting growth companies which attract high market valuations based on their perceived future potential, but history tells us that it is the profitable, cash-generative business that demonstrate persistence over decades. Examples of such businesses are Microsoft, Diageo, Coca Cola, Amazon and LVMH. Identifying companies which can become enduring champions from a crowded market takes a combination of wisdom, experience and a discipline that few professional investors exhibit in an industry driven by short-term relative performance.

Tacit portfolios are biased towards managers who have the courage to appear contrarian and unfashionable for the right reasons, and those are reasons rooted in deep financial analysis, an incisive assessment of the quality of a management team and its strategy, and an understanding of the fundamental principles of economics which tie company performance to the changing environment in which those businesses operate.

The majority of the companies listed on global stock markets do not achieve year-on-year consistency, not because they do not attempt to, but because external events create cyclical headwinds or tailwinds for the industries in which they operate. Conventionally, oil companies are an example of such businesses in people’s minds.

At Tacit, we believe that much of the recent volatility is in fact not driven by interest rate expectations, and will be seen in hindsight as the moment investors realised that many technology companies that they had believed would join the “20% club” are, in fact, more akin to BP. They have cyclical revenue and cost bases which means they cannot control as effectively as the less capital-intensive businesses we have highlighted above. Using one’s capital to supplement income only works if the cashflows replenish that capital. As many of our clients know, we focus very much on this potential mismatch when assessing their objectives and it is vital to understand this to protect against permanent impairment of capital.

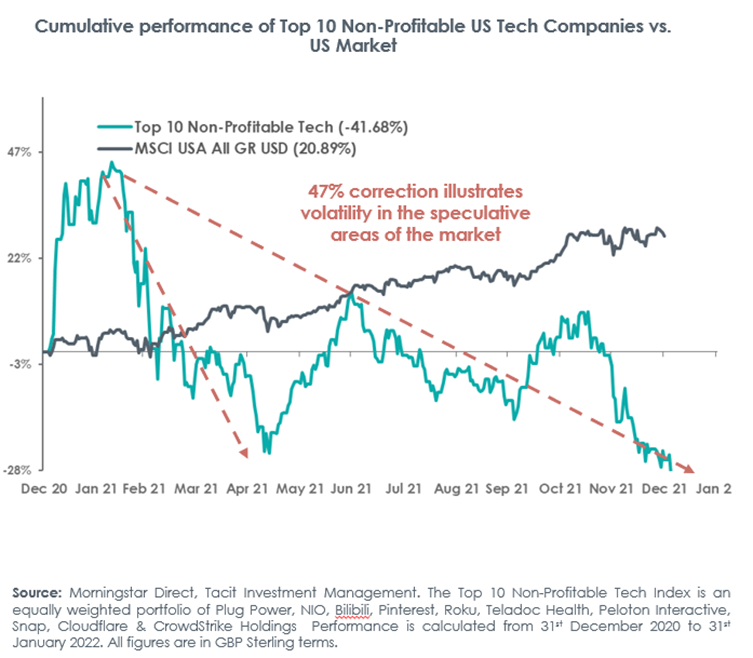

Very few businesses have managed to grow consistently over the longer term and investors need to remember that rather than following the short-term headlines. A company that can grow its free cash flows above inflation from year to year is rare, however during a period of free money many investors have forgotten this simple fact and the chart above only illustrates the beginning of this rotation in equity markets we believe.