Share this post

Late frosts

April, 2023

Gardeners among our readers will be very conscious of the damage a late frost can cause, especially if it has been preceded by clement weather which has encouraged buds to form and birds to settle down into comfortable nests. One night below freezing at just the wrong moment can devastate an apple harvest and spoil the anticipated show in an herbaceous border.

A not dissimilar anxiety is prevalent in investment markets at present. We have commented in previous Thoughts on the turn in the interest rate cycle and acknowledged that the rise from near-zero to above 4% has significant consequences for valuations across asset types. The higher discount rate, which is how economists term the yield on fixed interest instruments, has the effect of reducing the current price an investor will pay for future dividends. Put another way, if you can obtain around 3.5% in annual interest from a government bond which is underpinned by the tax raising powers of the government, why would you pay a premium for an uncertain dividend promise at an equivalent or even higher prospective yield?

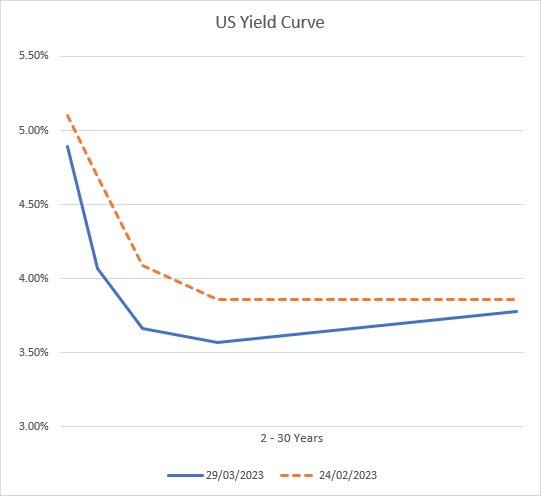

Fears of recession, brought on by high borrowing costs, lurk in the background, but economic activity is still positive even if it is anaemic. Investors fret and equity markets ebb and rise on a rotation between hopes that inflation, the spur to higher interest rates, is abating and that the interest rate cycle has peaked, and concern that central banks will tighten further. These shifts in investor outlook are demonstrated in the US Yield Curve below which moved significantly in the space of a month from an expectation of higher rates across the 30-year curve in late February to lower levels, particularly pronounced around the 10–12-year duration point.

We have emerged from a long period of unconventional central bank policy which forced interest rates down through Quantitative Easing, and a more recent period of fiscal stimulation (particularly marked in the US) which pumped money into the system. Both were intended to stave off recession, the former following the banking crisis of 2008/09 and the latter in response to the shock of Covid. Investment markets, arguably, became too dependent on interventions to maintain a benign environment of riskier assets. Short term traders will look for signs confirming that inflation has peaked and that interest rates will ease back, but they leave themselves vulnerable to a late frost, to turn the horticultural metaphor into an investment one.

Experienced gardeners know that not every plant in the border will be lost to an unseasonal cold snap. The flowering and fruiting season may be patchier than in previous years, but some plants may even flourish, giving a dazzling show later in the season. At Tacit, we avoid forecasting, and we do not set our strategies on expectations of short-term factors. Our central thesis is that the era of suppressed interest rates is over, for the present at least, and that investment decisions should be founded on the assumption that successful companies will adjust to a higher cost of capital and will be able to maintain their profit margins even though their costs have increased. What is required is thoughtful, selective investment and not a reliance on easing interest rates to float creaking vessels on a rising tide.

The potential of growing cashflows (and dividends) of well managed companies will maintain the real value of our clients’ wealth over time as history suggests that it is only equities that can provide inflation protection over the medium term to investors. Investors would do well to remember that, as with equities, higher interest rates today are not guaranteed either.