Share this post

Demographics

May, 2022

Demographics are deemed to be a driver of investment returns. The argument goes that the bigger the proportion of the population that is of a working age, the greater the economic value creation and the lower the drain on the public purse. These working people, then begin to save, providing a marginal buyer to equity markets as they have long time horizons and return requirements that outstrip cash deposit rates.

In the developed world, the previous generation of ‘wealth creators’ were dubbed the Baby Boomers, generally those individuals born between 1946 and 1964 and therefore aged between 57-75 years old. It is estimated that over 75 million births were recorded in the United States alone during this period.

As global investors, we believe that the sheer size of the populations in China and India will drive economic growth for many years to come, as it did in the US. The middle classes here will increase their spending as their incomes rise and this will provide the world with another pillar of growth. Size, however, isn’t the only important factor.

The recent inflationary issues in the US and Eurozone have illustrated quite clearly that governments need to carefully manage expectations as future tax revenues will be limited by demographic trends. ‘Money does not grow on trees’ as they say. It will become more evident that governments in countries such as the UK and France will not be able to increase the living standards of all. We have actually been living through this for over a decade, but it is only now people acknowledge it, as near zero interest rates have camouflaged the issue since 2008.

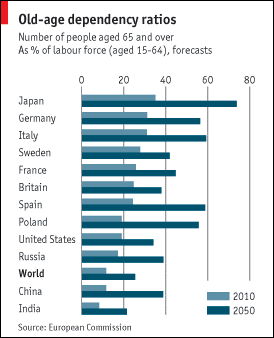

The chart below shows the old-age dependency ratios published by the European Commission on a regular basis and includes China and India. The ratio is a measure of the number of elderly people at an age when they are generally economically inactive (i.e., aged 65 and over), compared to the number of people of working age (i.e., 15-64 years old).

The interesting point which in our view is not really acknowledged by most global investors, is that the Chinese population is aging dramatically and that over the next 40 years, the dependency ratio will increase from 15 retirees for every 100 of working age to 39. This will impact policy and put pressure on the Chinese government to manage this position carefully, as increasing wealth and expectations of your population cannot be reversed as they get older. India and countries such as Indonesia on the other hand have the best demographic profiles of all of the countries shown above.

Tacit strategies have recently been realigned to take best advantage of this demographic trend as we believe the investment environment has materially altered for the future and we will be providing further insights into our thoughts over the coming weeks and months.